Small Business Financing & Loan Products

Explore financing options designed to support your business at every stage of growth.

Whether you are funding a fix and flip project, purchasing equipment, managing cash flow, or expanding operations, EZcash Shop helps small business owners explore financing options such as real estate-related financing, equipment financing, term loans, working capital, and SBA loans-based on eligibility and business needs.

Which Business Financing Option is Right for Your Company?

Every business is different, and small business financing options are not one-size-fits-all. The right business loan or funding solution depends on factors such as your revenue, time in business, cash flow, credit profile, and how you plan to use the funds. Below, we outline common business financing products we work with our clients on, along with typical use cases for each, to help you better understand which option may fit your situation. Final eligibility, terms, rates, and approvals are determined by the lender.

Fix & Flip Financing for Real Estate Investors

Fix and flip financing is a short-term real estate investment loan designed for investors who purchase, renovate and resell residential properties. Unlike traditional business loans, fix and flip loans are based primarily on the property's value and projected after-repair value (ARV), rather than borrower income alone.

These loans are commonly used for time-sensitive investment opportunities and can include both purchase and renovation costs, with faster approvals and flexible repayment terms.

Common uses for fix & flip financing include:

- Purchasing distressed or undervalued properties

- Funding renovation and rehab costs

- Short-term investment projects with resale or refinance exits

Learn more about Fix & Flip Financing -> Fix & Flip Financing.

Equipment Financing

Equipment financing allows businesses to purchase or upgrade equipment by spreading the cost over time, with the equipment itself typically serving as collateral. This type of business loan helps preserve cash flow while enabling companies to invest in the tools, vehicles, and machinery needed to operate and grow.

Example:

A manufacturing company uses equipment financing to purchase new production machinery, increasing output while making manageable monthly payments as customer orders are fulfilled.

Equipment Financing Overview:

- Loan designed specifically for equipment purchases, with the equipment used as collateral.

- Typically offers lower interest rates and longer repayment terms than unsecured term loans or business lines of credit.

- Interest rates are often higher than SBA loans, but approval is faster and requirements are simpler.

- Best for vehicles, machinery, heavy equipment, and business assets with clear resale value.

- Use of funds is restricted to the approved equipment, unlike general-purpose term loans or LOCs.

- Usually requires equipment invoices, vendor information, and sometimes serial numbers.

- Faster approval than SBA loans but slower than unsecured term loans or lines of credit.

- Payments are generally fixed, providing predictable monthly costs and often lower payments due to longer terms.

Learn more about equipment financing -> Equipment Financing.

Term Loans for Small Businesses

A small business term loan provides a company with a one-time lump sum of capital that is repaid in regular payments over a fixed period of time. Term loans are commonly used for planned, long-term investments such as expanding operations, purchasing equipment, renovating a location, or consolidating existing business debt.

Example:

A construction company uses a business term loan to purchase new equipment and take on larger projects, repaying the loan over time as jobs are completed and revenue is generated.

Overview of Term Loans:

- Lump sum funding provided upfront.

- Longer repayment terms, typically 1–5 years (sometimes longer).

- Monthly payments in most cases.

- Best suited for long-term business investments, including:

* Equipment purchases

* Business Expansion

* Renovations or build-outs

* Major one-time expenses

- Often offers lower interest rates compared to short-term financing due to longer terms and reduced lender risk.

Not sure if a term loan is the right fit? EZcash Shop helps business owners compare multiple financing options to find the solution that best aligns with their goals and cash flow.

Lines of Credit for Businesses

A business line of credit provides flexible access to funds that a business can draw from as needed, up to a pre-approved limit. You only pay interest on the amount you actually use, making it an efficient solution for managing cash flow, covering short-term expenses, or handling unexpected costs.

How a Business Line of Credit Works

- A line of credit is a form of revolving credit, meaning you can:

- Borrow funds

- Repay what you've used

- Borrow again as needed (up to the limit)

This flexibility makes lines of credit ideal for businesses with ongoing or variable expenses

Example:

A doctor’s office uses a business line of credit to cover payroll and operating expenses while waiting for insurance reimbursements. Once receivables are collected, the balance is paid down, freeing up credit for future use.

Key Features of a Business Line of Credit

Revolving credit: — Borrow, repay, and reuse funds without reapplying.

Interest charged only on funds used: Unlike term loans, interest does not apply to the full credit limit.

Flexible access: No single lump-sum disbursement.

Ideal for ongoing or unpredictable expenses: Such as payroll, inventory, or operating costs.

Typically shorter-term and smaller limits than traditional term loans.

Often variable interest rates, compared to fixed payments on term loans.

Stronger credit and financials required than many short-term financing options, often similar to term loan standards.

SBA Loans

An SBA loan is a business loan partially guaranteed by the U.S. Small Business Administration, helping lenders offer lower interest rates, longer repayment terms, and more flexible financing options to qualified small businesses. SBA loans are commonly used for business growth, commercial real estate, equipment purchases, acquisitions, and refinancing existing debt.

Example:

An accounting firm uses an SBA loan to purchase a larger office space hire additional staff, repaying the loan over time with predictable monthly payments.

SBA Loan Overview:

Government-backed business loans issued by banks and SBA-approved lenders to reduce lender risk.

Typically offer lower interest rates and longer repayment terms than conventional term loans or business lines of credit.

Ideal for large, long-term investments, including business expansion, real estate, equipment, or debt refinancing.

More structured and restrictive use of funds compared to traditional term loans and lines of credit.

Slower approval process due to SBA documentation and compliance requirements.

Often require strong financials, good personal and business credit, and detailed records (tax returns, financial statements).

May require personal guarantees and, in some cases, collateral.

Working Capital Loans

A working capital loan helps businesses cover day-to-day operating expenses and manage short-term cash flow needs. It is commonly used to bridge gaps between outgoing expenses and incoming revenue, especially for businesses with seasonal or fluctuating sales cycles.

Example:

An e-commerce company uses a working capital loan to purchase inventory and fund online advertising ahead of a peak sales season, then repays the loan as customer orders are fulfilled and revenues is collected.

Overview:

- Short-term business financing designed to support daily operations and cash flow management.

- Typically funded as a lump sum, unlike a revolving business line of credit.

- Fastest approval and funding compared to term loans, equipment financing, and SBA loans.

- Generally higher cost than term loans, lines of credit, equipment financing, and SBA loans due to speed and shorter repayment terms.

- Best for payroll, inventory, marketing, covering slow periods, or urgent business expenses.

- Often requires less documentation and offers more flexible underwriting standards.

- Shorter repayment terms, frequently with weekly or daily payments.

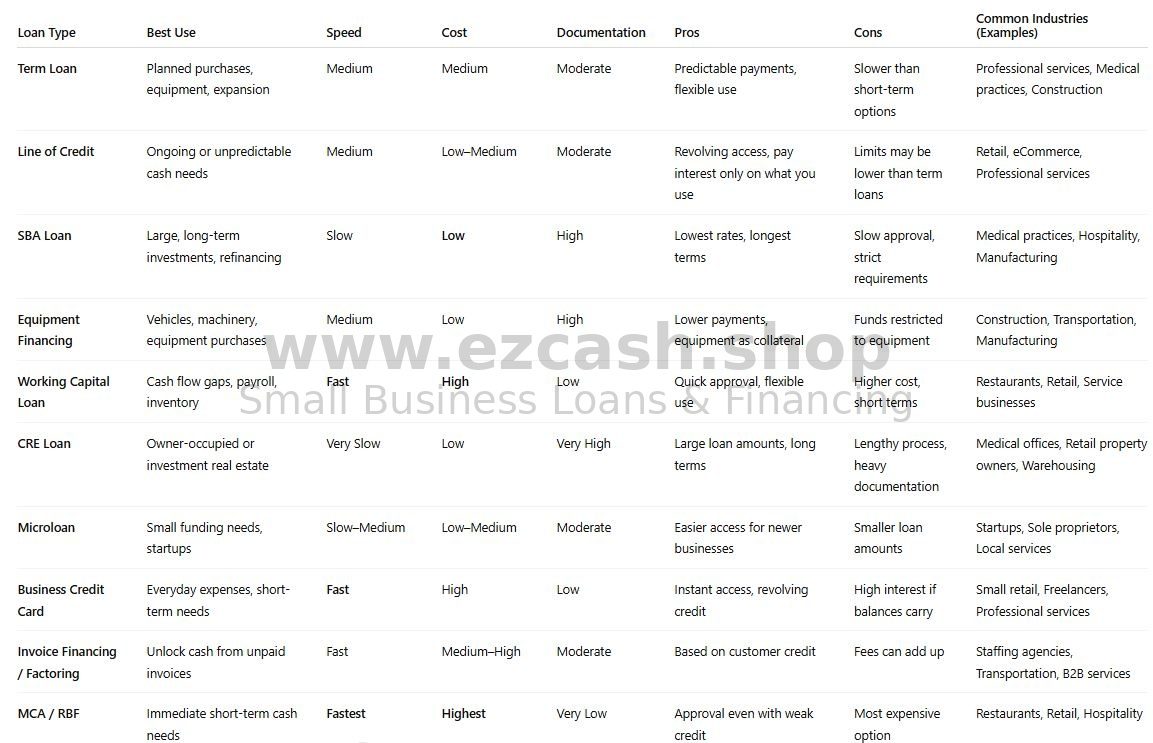

COMPARISON TABLE BY LOAN TYPE

How to Choose the Right Business Financing Option

Different types of business financing are designed for different needs. The right option depends on how you plan to use the funds, how quickly you need them, and how you prefer to repay.

If you’re making a planned purchase or investment, such as equipment or expansion, a term loan can provide predictable monthly payments and flexible use of funds. For businesses that need ongoing access to capital to manage cash flow fluctuations, a line of credit offers revolving access, allowing you to borrow and repay as needed.

For larger, long-term investments or refinancing, SBA loans and commercial real estate (CRE) loans typically offer the lowest rates and longest terms, but they also involve more documentation and longer approval timelines. These options are generally best for established businesses with strong financials and a longer planning horizon.

When the need is equipment-specific, such as vehicles or machinery, equipment financing can provide lower payments because the equipment itself serves as collateral. For businesses facing short-term cash flow gaps, working capital loans offer fast access to funds, though they usually come with higher costs and shorter repayment terms.

Smaller businesses or startups with modest funding needs may benefit from microloans, while business credit cards can be useful for everyday expenses and short-term spending if balances are managed carefully. Companies with outstanding invoices may consider invoice financing or factoring to unlock cash tied up in receivables.

Finally, merchant cash advances (MCA) or revenue-based financing (RBF) provide very fast access to capital and are repaid based on sales, but they are typically the most expensive option and are best used cautiously for short-term needs.

Bottom line

Each financing option involves a tradeoff between speed, cost, flexibility, and documentation. Understanding your business’ cash flow, timing, and repayment comfort can help you narrow down which option may be the best fit.

Financing options, terms, and eligibility vary by lender and individual business qualifications.

Take the first step—contact EZcash Shop today to explore your small business financing options.